Compare Conditional Variance Model Fit Statistics Using Econometric Modeler App

This example shows how to specify and fit GARCH, EGARCH, and GJR

models to data using the Econometric Modeler app. Then, the example determines the

model that fits to the data the best by comparing fit statistics. The data set,

which is stored in Data_FXRates.mat, contains foreign exchange

rates measured daily from 1979–1998.

Consider creating a predictive model for the Swiss franc to US dollar exchange

rate (CHF).

Import Data into Econometric Modeler

At the command line, load the Data_FXRates.mat data

set.

load Data_FXRatesAt the command line, open the Econometric Modeler app.

econometricModeler

Alternatively, open the app from the apps gallery (see Econometric Modeler).

Import DataTimeTable into the app:

On the Modeler tab, in the Import section, click the Import button

.

.In the Import Data dialog box, select the check box for the

DataTimeTablevariable.Click Import.

All time series variables in DataTimeTable appear in the

Time Series pane, and a time series plot of all the

series appears in the Plot(AUD) figure window.

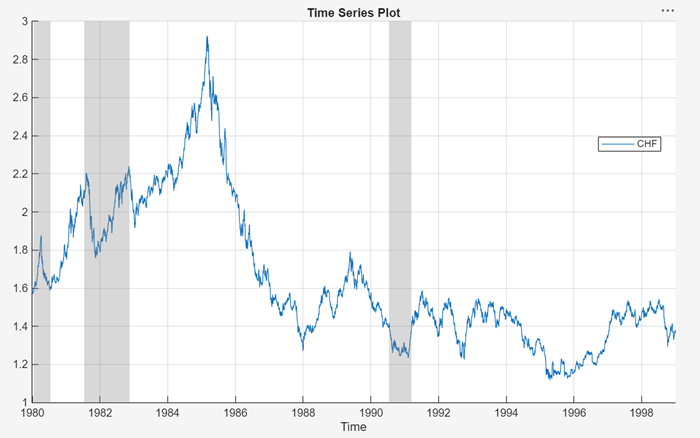

Plot the Series

Plot the Swiss franc exchange rates by double-clicking the

CHF time series in the Time

Series pane.

Highlight periods of recession:

In the Plot(CHF) figure window, right-click the plot.

In the context menu, select Show Recessions.

The CHF series appears to have a stochastic

trend.

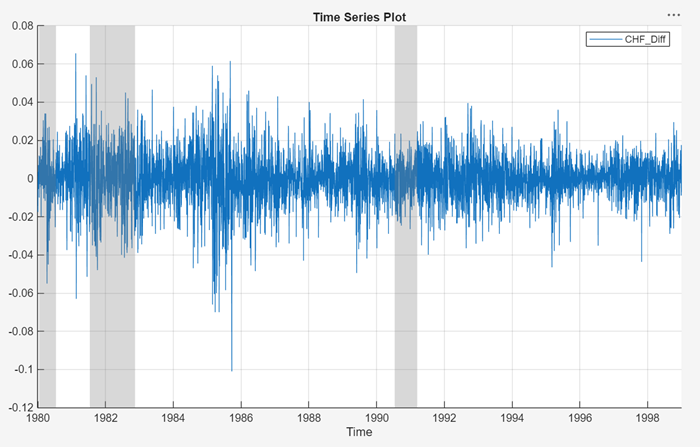

Stabilize the Series

Stabilize the Swiss franc exchange rates by applying the first difference to

CHF.

In the Time Series pane, select

CHF.On the Modeler tab, in the Transforms section, click Difference.

A variable named CHF_Diff, representing the

differenced series, appears in the Time Series pane, its

value appears in the Preview pane, and its time series plot

appears in the Plot(CHF_Diff) figure window.

The series appears to be stable, but it exhibits volatility clustering.

Assess Presence of Conditional Heteroscedasticity

Test the stable Swiss franc exchange rate series for conditional heteroscedasticity by conducting Engle's ARCH test. Run the test assuming an ARCH(1) alternative model, then run the test again assuming an ARCH(2) alternative model. Maintain an overall significance level of 0.05 by decreasing the significance level of each test to 0.05/2 = 0.025.

In the Time Series pane, select

CHF_Diff.On the Modeler tab, in the Tests section, click Add Test > Engle's ARCH Test.

On the ARCH tab, in the Settings section, set Number of Lags of

1.Set Significance Level to

0.025.In the Tests section, click Run Test.

Repeat steps 3 through 5, but set Number of Lags to

2instead.

The test results appear in the Results table of the ARCH(CHF_Diff) document.

The tests reject the null hypothesis of no ARCH effects against the

alternative models. This result suggests specifying a conditional variance model

for CHF_Diff containing at least two ARCH lags.

Conditional variance models with two ARCH lags are locally equivalent to models

with one ARCH and one GARCH lag. Consider GARCH(1,1), EGARCH(1,1), and GJR(1,1)

models for CHF_Diff.

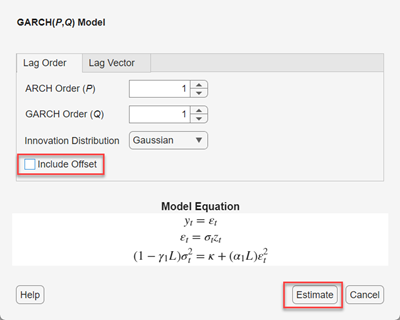

Estimate GARCH Model

Specify a GARCH(1,1) model and fit it to the

CHF_Diff series.

In the Time Series pane, select the

CHF_Difftime series.Click the Modeler tab. Then, in the Models section, click the arrow to display the models gallery.

In the models gallery, in the GARCH Models section, click GARCH.

In the GARCH Model Parameters dialog box, on the Lag Order tab, clear the Include Offset check box, then click Estimate.

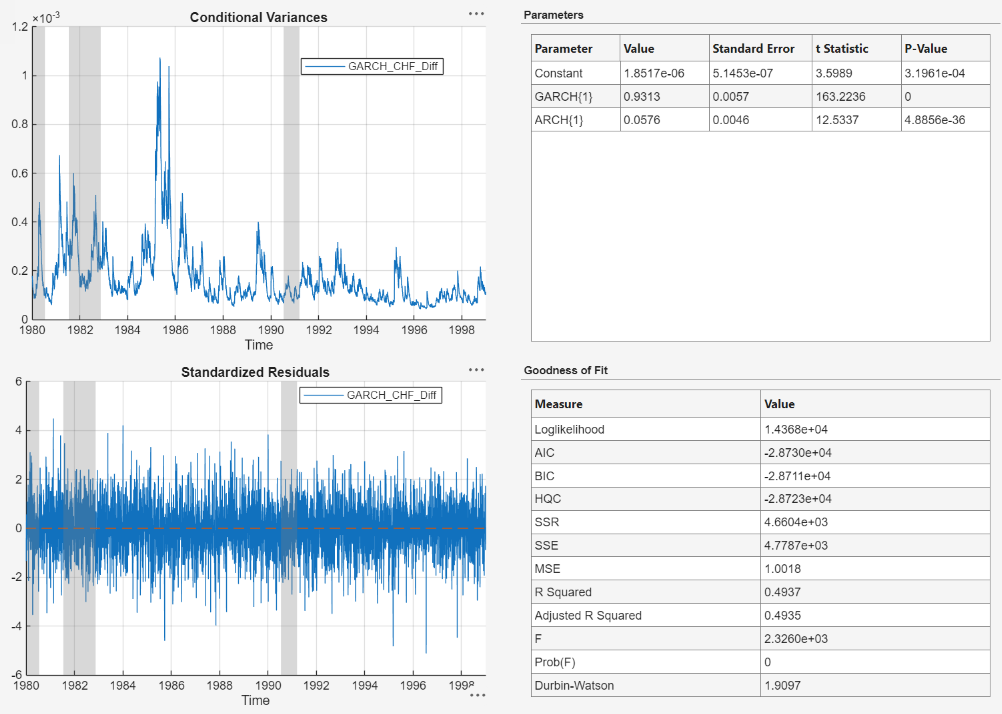

The model variable GARCH_CHF_Diff appears in the Models pane, its value appears in the Preview pane, and its estimation summary appears in the Fit(GARCH_CHF_Diff) document.

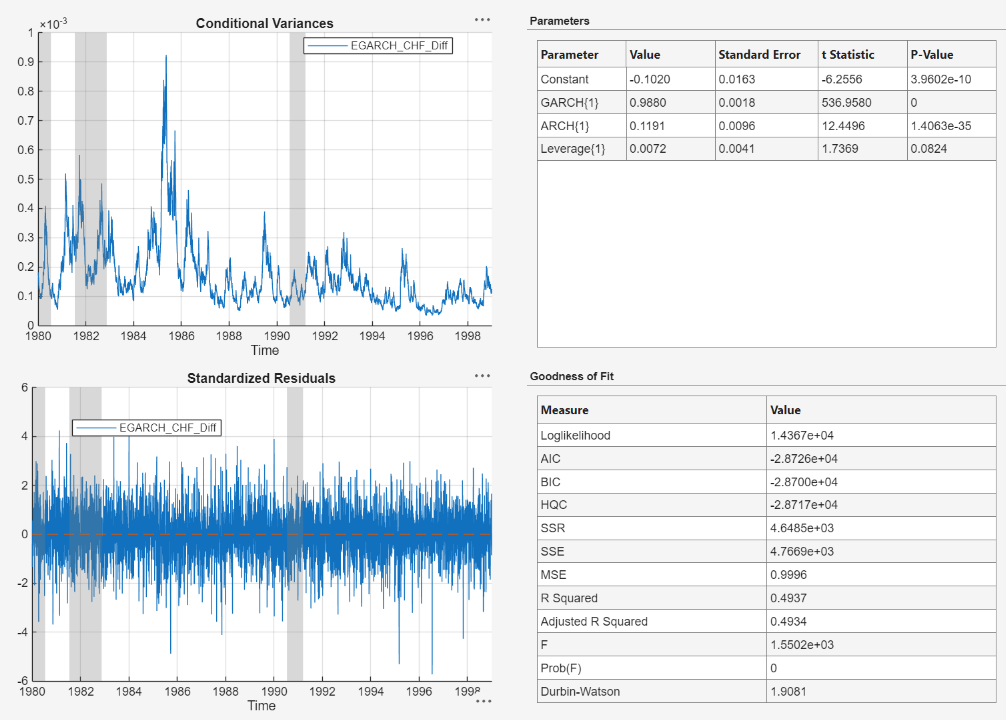

Specify and Estimate EGARCH Model

Specify an EGARCH(1,1) model containing a leverage term at the first lag, and

fit the model to the CHF_Diff series.

In the Time Series pane, select the

CHF_Difftime series.On the Modeler tab, in the Models section, click the arrow to display the models gallery.

In the models gallery, in the GARCH Models section, click EGARCH.

In the EGARCH Model Parameters dialog box, on the Lag Order tab, clear the Include Offset check box, then click Estimate.

Econometric Modeler includes a leverage lag for each ARCH lag. You can remove or adjust leverage lags on the Lag Vector tab.

The model variable EGARCH_CHF_Diff appears in the Models pane, its value appears in the Preview pane, and its estimation summary appears in the Fit(EGARCH_CHF_Diff) document.

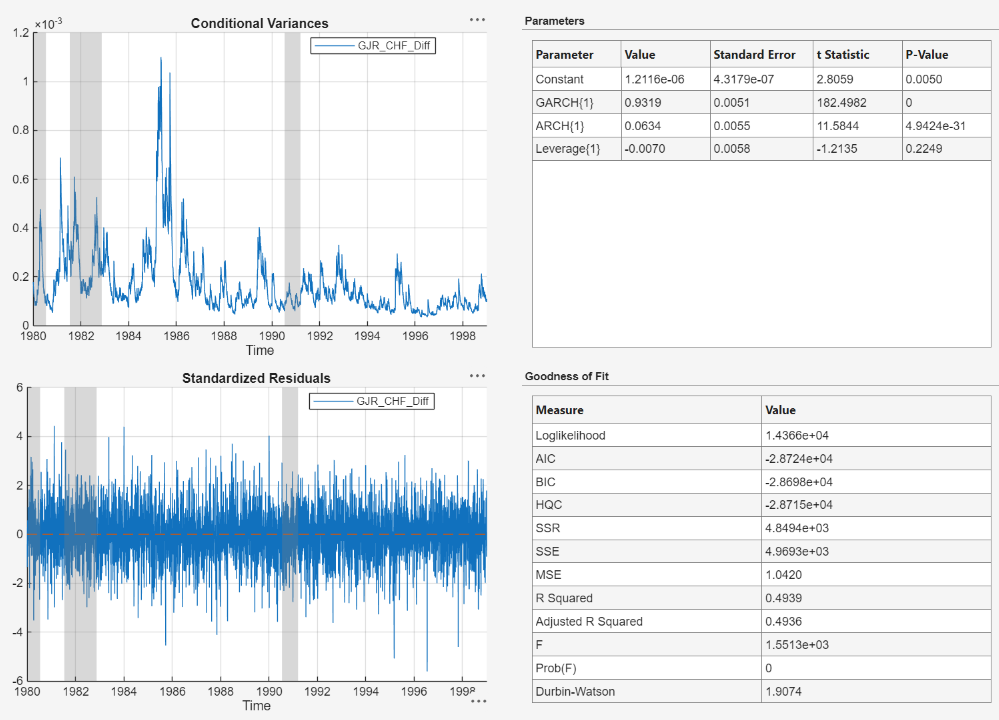

Specify and Estimate GJR Model

Specify a GJR(1,1) model containing a leverage term at the first lag, and fit

the model to the CHF_Diff series.

In the Time Series pane, select the

CHF_Difftime series.On the Modeler tab, in the Models section, click the arrow to display the models gallery.

In the models gallery, in the GARCH Models section, click GJR.

In the GJR Model Parameters dialog box, on the Lag Order tab, clear the Include Offset check box, then click Estimate.

Econometric Modeler includes a leverage lag for each ARCH lag. You can remove or adjust leverage lags on the Lag Vector tab.

The model variable GJR_CHF_Diff appears in the Models pane, its value appears in the Preview pane, and its estimation summary appears in the Fit(GJR_CHF_Diff) document.

Choose Model

Choose the model with the best parsimonious in-sample fit. Base your decision on the model yielding the minimal Akaike information criterion (AIC). The table shows the AIC fit statistics of the estimated models, as given in the Goodness of Fit section of the estimation summary of each model.

| Model | AIC |

|---|---|

| GARCH(1,1) | -28730 |

| EGARCH(1,1) | -28726 |

| GJR(1,1) | -28724 |

The GARCH(1,1) model yields the minimal AIC value. Therefore, it has the best parsimonious in-sample fit of all the estimated models.