Pubblicato

Modeling Carbon Emissions: An Econometric Approach

In a recent webinar hosted by MathWorks, we were joined by Andy Cates, a senior economist at Haver Analytics, one of our...

oltre un anno fa

Pubblicato

Deep Learning in Quantitative Finance: Multiagent Reinforcement Learning for Financial Trading

The following blog was written by Adam Peters, Software Engineer at Mathworks. Download the code for this example from...

quasi 2 anni fa

Pubblicato

Key Insights from our Executive Panel Discussion: Addressing Climate Risk through effective Stress Testing, Reporting, and Governance

Background In the rapidly evolving landscape of financial risk management, addressing climate risk has emerged as a...

circa 2 anni fa

Pubblicato

MATLAB Portfolio Backtesting – A new app now on GitHub!

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. MathWorks has a new...

circa 2 anni fa

Pubblicato

Top MATLAB Quantitative Finance Resources now on GitHub

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. MathWorks now has a...

circa 2 anni fa

Pubblicato

Model Monitoring and Drift Detection with Modelscape

MathWorks recently hosted a webinar on Model Monitoring and Drift Detection, where Paul Peeling presented strategies for...

circa 2 anni fa

Pubblicato

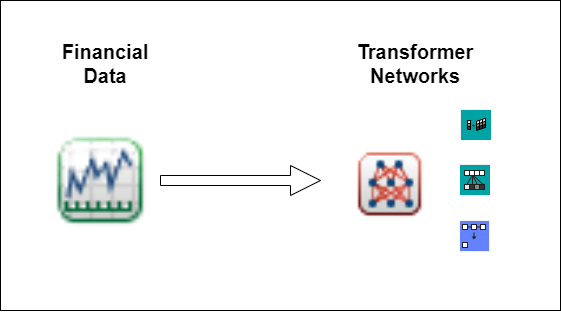

Deep Learning in Quantitative Finance: Transformer Networks for Time Series Prediction

The following blog was written by Owen Lloyd , a Penn State graduate who recently join the MathWorks Engineering...

circa 2 anni fa

Pubblicato

Climate Risk in Finance: Insights from Our Comprehensive Executive Panel Discussion

The following blog was written by Arpit Narain from the MathWorks Finance team. 1. Introduction In today’s financial...

circa 2 anni fa

Pubblicato

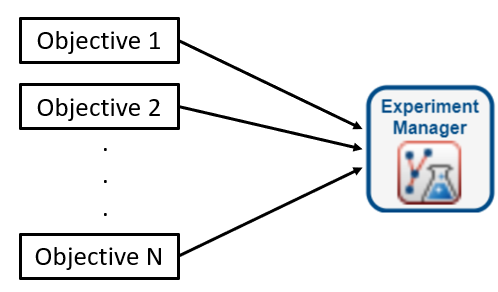

Managing and Fine-Tuning Portfolio Optimization Workflows with Experiment Manager

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. The code used to develop...

oltre 2 anni fa

Pubblicato

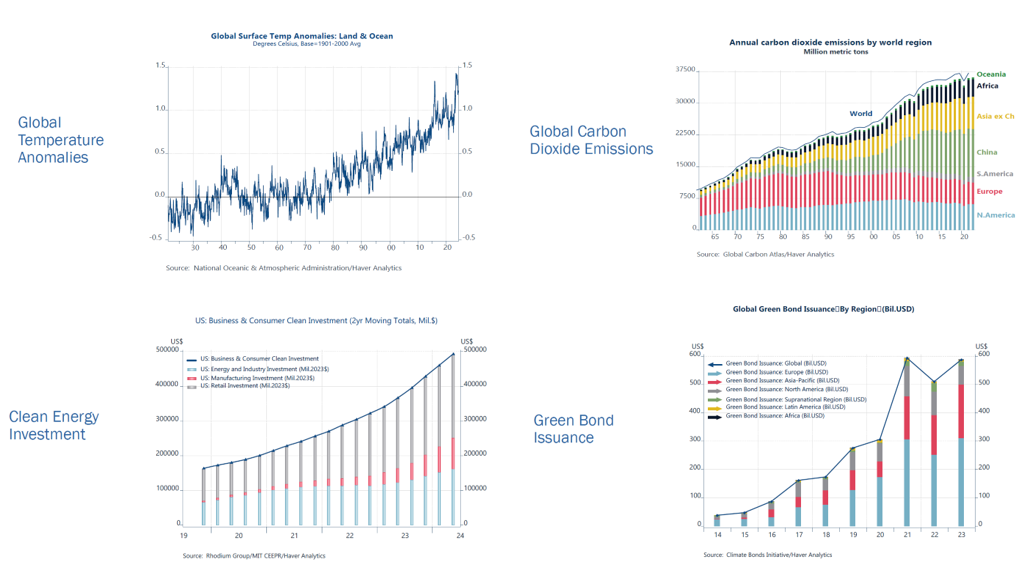

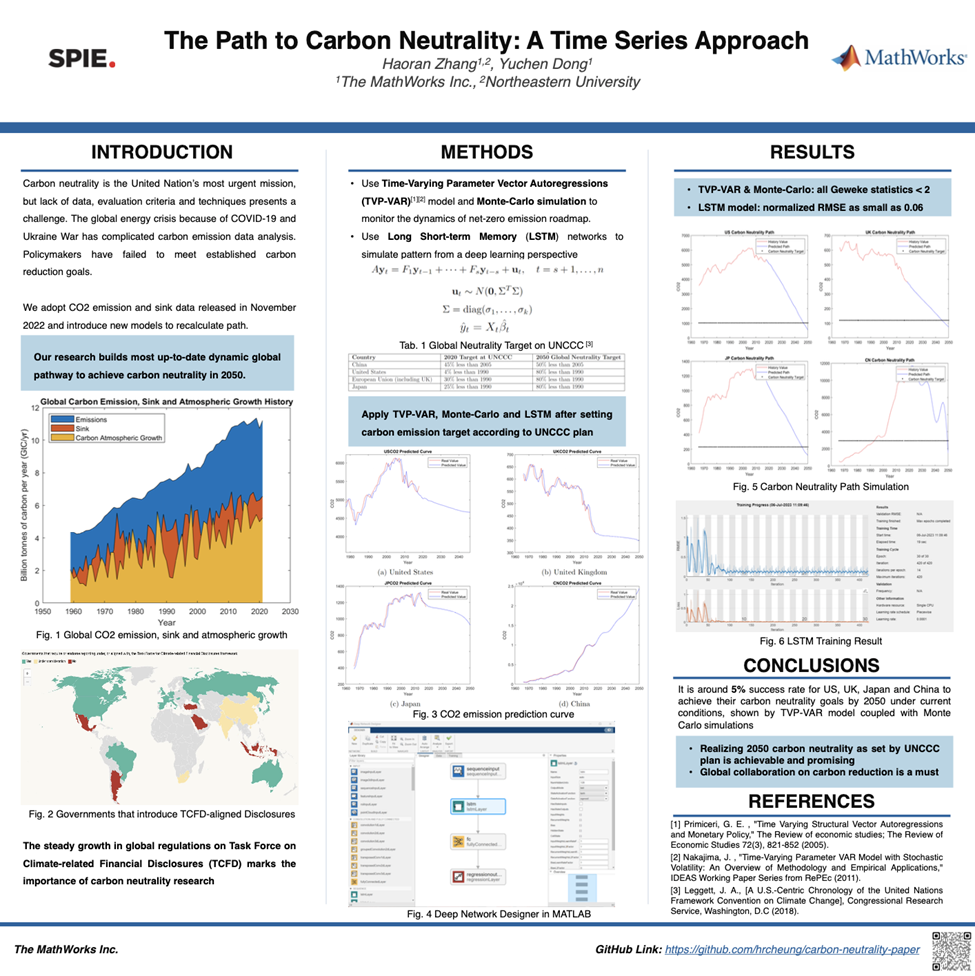

The Path to Carbon Neutrality: A Time Series Approach

The following blog was written by Leslie Zhang, a Northeastern graduate who recently joined MathWorks Engineering...

oltre 2 anni fa

Pubblicato

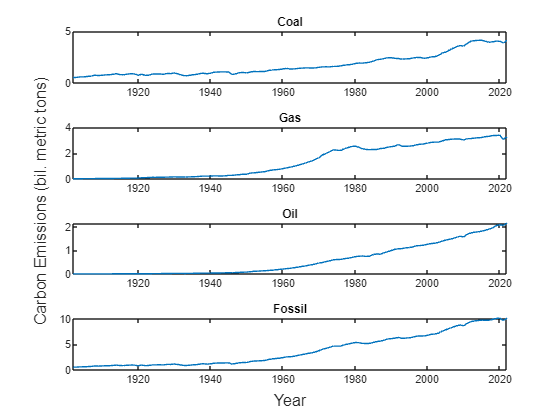

Time Series Analysis of Trends in Global Carbon Emissions from Fossil Fuels

The following post is from Hang Qian, Software Developer on the Econometrics Toolbox Team. Global carbon emissions have...

oltre 2 anni fa

Pubblicato

MathWorks Finance Conference 2023

It’s my pleasure to give everyone a sneak peek into the upcoming MathWorks Finance 2023 conference, which will be held...

oltre 2 anni fa

Pubblicato

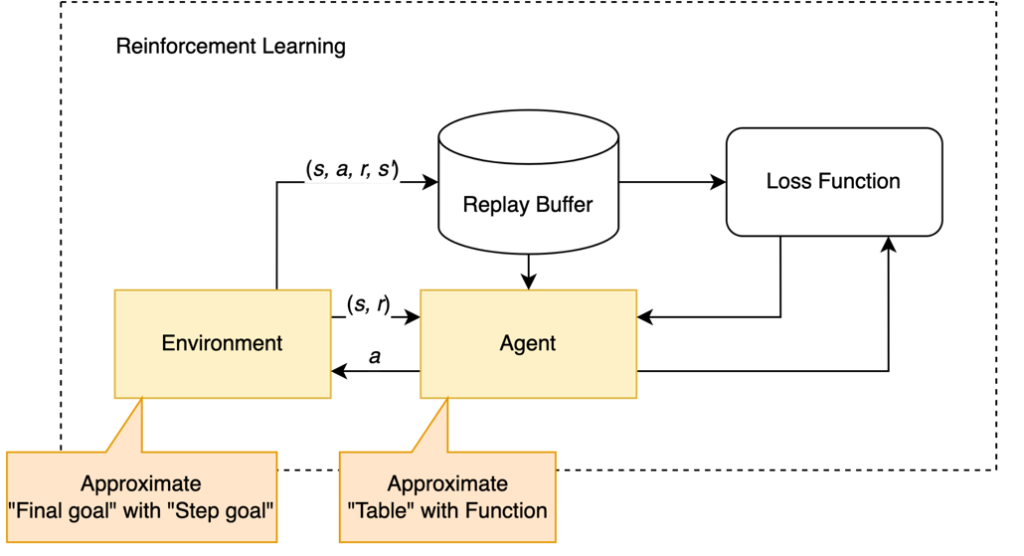

Reinforcement Learning as your portfolio advisor

The following post is from Ian Chie, Bowen Fang, Botao Zhang and Yichen Yao from Columbia University. Inspiration Let’s say...

oltre 2 anni fa

Pubblicato

Quantum Computing for Optimizing Investment Portfolios

The following post is from Sofia Ma, Senior Engineer for Finance Quantum computing is a cutting-edge field of study that...

oltre 2 anni fa

Pubblicato

The evolution of Quantitative Finance in MATLAB (What’s New)

Hi Everyone, I would like to welcome you to our new blog on Quantitative Finance. To kick things off, I’d like to give an...

quasi 3 anni fa