Estimate Regression Model with ARIMA Errors

This example shows how to estimate the sensitivity of the US Gross Domestic Product (GDP) to changes in the Consumer Price Index (CPI) using estimate.

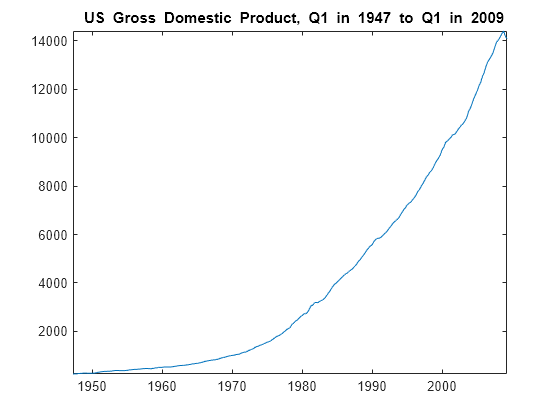

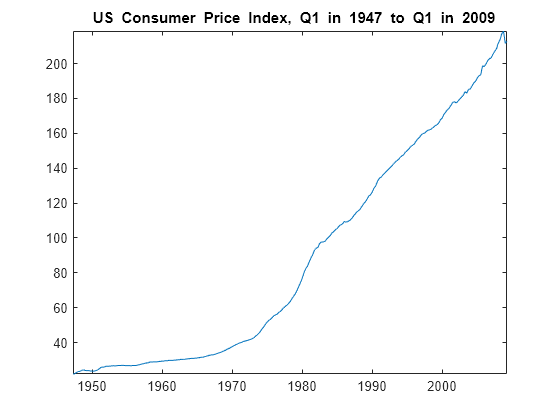

Load the US macroeconomic data set, Data_USEconModel. Plot the GDP and CPI.

load Data_USEconModel gdp = DataTimeTable.GDP; cpi = DataTimeTable.CPIAUCSL; figure plot(DataTimeTable.Time,gdp) title("{\bf US Gross Domestic Product, Q1 in 1947 to Q1 in 2009}") axis tight

figure plot(DataTimeTable.Time,cpi) title("{\bf US Consumer Price Index, Q1 in 1947 to Q1 in 2009}") axis tight

gdp and cpi seem to increase exponentially.

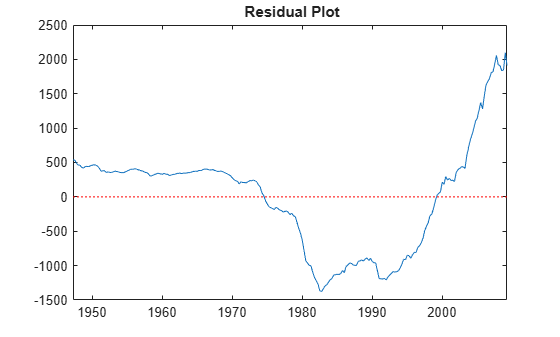

Regress gdp onto cpi. Plot the residuals.

XDes = [ones(length(cpi),1) cpi]; % Design matrix beta = XDes\gdp; u = gdp - XDes*beta; % Residuals figure plot(DataTimeTable.Time,u) h1 = gca; hold on plot(h1.XLim,[0 0],"r:") title("{\bf Residual Plot}") hold off

The pattern of the residuals suggests that the standard linear model assumption of uncorrelated errors is violated. The residuals appear autocorrelated.

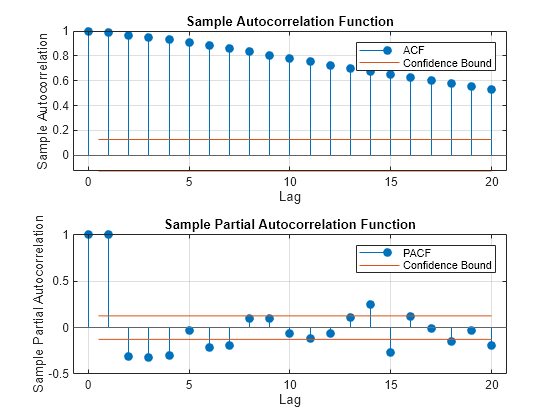

Plot correlograms for the residuals.

figure tiledlayout(2,1) nexttile autocorr(u) nexttile parcorr(u)

The autocorrelation function suggests that the residuals are a nonstationary process.

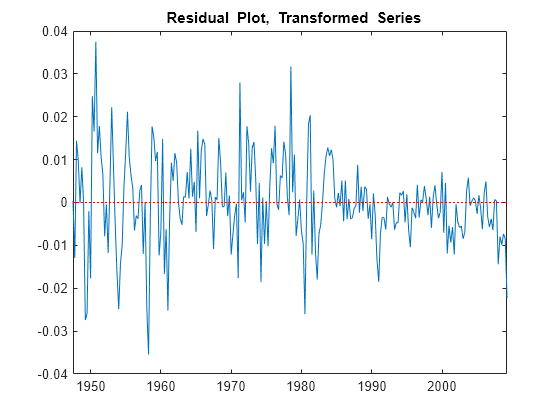

Apply the first difference to the logged series to stabilize the residuals.

dlGDP = diff(log(gdp)); dlCPI = diff(log(cpi)); dlXDes = [ones(length(dlCPI),1) dlCPI]; beta = dlXDes\dlGDP; u = dlGDP - dlXDes*beta; figure plot(DataTimeTable.Time(2:end),u); h2 = gca; hold on plot(h2.XLim,[0 0],"r:") title("{\bf Residual Plot, Transformed Series}") hold off

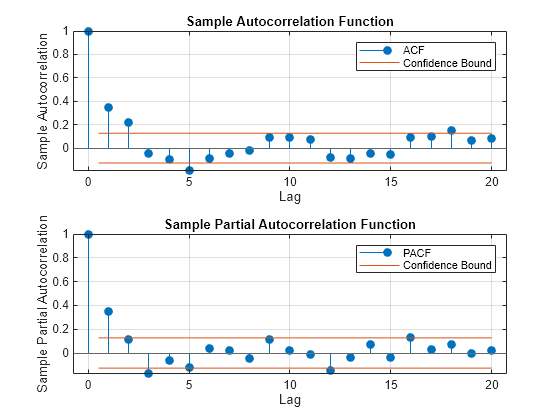

figure tiledlayout(2,1) nexttile autocorr(u) nexttile parcorr(u)

The residual plot from the transformed data suggests stabilized, albeit heteroscedastic, unconditional disturbances. The correlograms suggest that the unconditional disturbances follow an AR(1) process.

Specify the regression model with AR(1) errors:

Mdl = regARIMA(ARLags=1);

estimate estimates any parameter having a value of NaN.

Fit Mdl to the data.

EstMdl = estimate(Mdl,dlGDP,X=dlCPI,Display="params");

Regression with ARMA(1,0) Error Model (Gaussian Distribution):

Value StandardError TStatistic PValue

__________ _____________ __________ __________

Intercept 0.012762 0.0013472 9.4734 2.7098e-21

AR{1} 0.38245 0.052494 7.2856 3.2031e-13

Beta(1) 0.3989 0.077286 5.1614 2.4515e-07

Variance 9.0101e-05 5.947e-06 15.151 7.5075e-52

Alternatively, estimate the regression coefficients and Newey-West standard errors using hac.

hac(dlCPI,dlGDP,Intercept=true,Display="full");Estimator type: HAC

Estimation method: BT

Bandwidth: 4.1963

Whitening order: 0

Effective sample size: 248

Small sample correction: on

Coefficient Estimates:

| Coeff SE

------------------------

Const | 0.0115 0.0012

x1 | 0.5421 0.1005

Coefficient Covariances:

| Const x1

--------------------------

Const | 0.0000 -0.0001

x1 | -0.0001 0.0101

The intercept estimates are close, but the regression coefficient estimates corresponding to dlCPI are not. This is because regARIMA explicitly models for the autocorrelation of the disturbances. hac estimates the coefficients using ordinary least squares, and returns standard errors that are robust to the residual autocorrelation and heteroscedasticity.

Assuming that the model is correct, the results suggest that an increase of one point in the CPI rate increases the GDP growth rate by 0.399 points. This effect is significant according to the t statistic.

From here, you can use forecast or simulate to obtain forecasts and forecast intervals for the GDP rate. You can also compare several models by computing their AIC statistics using aicbic.

See Also

estimate | forecast | simulate | aicbic