Noncentral F Distribution

Definition

Similar to the noncentral χ2 distribution, the toolbox calculates noncentral F distribution probabilities as a weighted sum of incomplete beta functions using Poisson probabilities as the weights.

The noncentral F distribution cumulative distribution function is

for x ≥ 0, where I(x|a,b) is the regularized incomplete beta function with parameters a and b, and δ is the noncentrality parameter.

Background

As with the χ2 distribution, the F distribution is a special case of the noncentral F distribution. The F distribution is the result of taking the ratio of χ2 random variables each divided by its degrees of freedom.

If the numerator of the ratio is a noncentral chi-square random variable divided by its degrees of freedom, the resulting distribution is the noncentral F distribution.

The main application of the noncentral F distribution is to calculate the power of a hypothesis test relative to a particular alternative.

Examples

Compute Noncentral F Distribution Probability Density Function

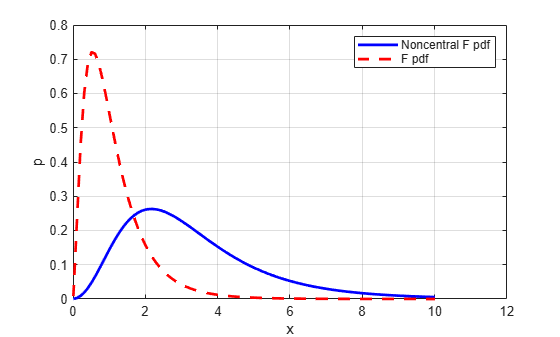

Compute the probability density function (pdf) of a noncentral F distribution with the numerator degrees of freedom nu1=5, denominator degrees of freedom nu2=20, and noncentrality parameter delta=10. For comparison, also compute the pdf of an F distribution with the same degrees of freedom.

x = 0.01:0.1:10.01; nu1 = 5; nu2 = 20; delta = 10; ncf = ncfpdf(x,nu1,nu2,delta); f = fpdf(x,nu1,nu2);

Plot the noncentral F pdf and the F pdf on the same figure.

figure plot(x,ncf,"b-",LineWidth=2) hold on grid on plot(x,f,"r--",Linewidth=2) xlabel("x") ylabel("p") legend("Noncentral F pdf","F pdf") hold off

See Also

ncfcdf | ncfpdf | ncfinv | ncfstat | ncfrnd | random