filter

Filter disturbances through vector error-correction (VEC) model

Syntax

Description

Y = filter(Mdl,Z)Y containing the multivariate

response series, which results from filtering the underlying input numeric array

Z containing the multivariate disturbance series. The

series in Z are associated with the model innovations

process through the fully specified VEC(p – 1) model

Mdl.

Tbl2 = filter(Mdl,Tbl1,Presample=Presample)Tbl2 containing the multivariate response series, which results from filtering the underlying multivariate disturbance series in the input table or timetable Tbl1. filter initializes the response series using the required table or timetable of presample data in Presample. Variables in Tbl1 are associated with the model innovations process through Mdl. (since R2022b)

filter selects the variables in Mdl.SeriesNames or all variables in Tbl1. To select different disturbance variables in Tbl1 to filter through the model, use the DisturbanceVariables name-value argument. filter selects the same variables for Presample by default, but you can select different variables by using the PresampleResponseVariables name-value argument.

[___] = filter(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name,Value)filter returns the output argument combination for the

corresponding input arguments. For example, filter(Mdl,Z,Y0=PS,X=Exo) filters

the numeric array of disturbances Z through the

VEC(p – 1) model Mdl, and specifies

the numeric array of presample response data PS and the

numeric matrix of exogenous predictor data Exo for the model

regression component.

Examples

Consider a VEC model for the following seven macroeconomic series. Then, fit the model to the data and filter disturbances through the fitted model. Supply the disturbances as a numeric matrix.

Gross domestic product (GDP)

GDP implicit price deflator

Paid compensation of employees

Nonfarm business sector hours of all persons

Effective federal funds rate

Personal consumption expenditures

Gross private domestic investment

Suppose that a cointegrating rank of 4 and one short-run term are appropriate, that is, consider a VEC(1) model.

Load the Data_USEconVECModel data set.

load Data_USEconVECModelFor more information on the data set and variables, enter Description at the command line.

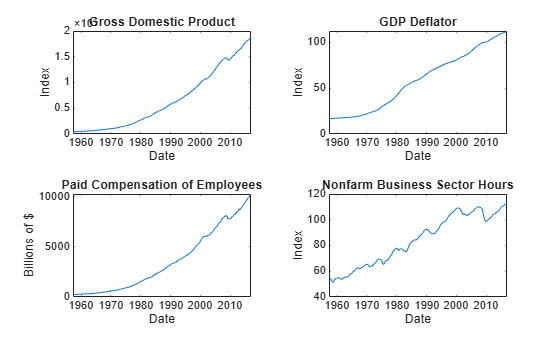

Determine whether the data needs to be preprocessed by plotting the series on separate plots.

figure tiledlayout(2,2) nexttile plot(FRED.Time,FRED.GDP) title("Gross Domestic Product") ylabel("Index") xlabel("Date") nexttile plot(FRED.Time,FRED.GDPDEF) title("GDP Deflator") ylabel("Index") xlabel("Date") nexttile plot(FRED.Time,FRED.COE) title("Paid Compensation of Employees") ylabel("Billions of $") xlabel("Date") nexttile plot(FRED.Time,FRED.HOANBS) title("Nonfarm Business Sector Hours") ylabel("Index") xlabel("Date")

figure tiledlayout(2,2) nexttile plot(FRED.Time,FRED.FEDFUNDS) title("Federal Funds Rate") ylabel("Percent") xlabel("Date") nexttile plot(FRED.Time,FRED.PCEC) title("Consumption Expenditures") ylabel("Billions of $") xlabel("Date") nexttile plot(FRED.Time,FRED.GPDI) title("Gross Private Domestic Investment") ylabel("Billions of $") xlabel("Date")

Stabilize all series, except the federal funds rate, by applying the log transform. Scale the resulting series by 100 so that all series are on the same scale.

FRED.GDP = 100*log(FRED.GDP); FRED.GDPDEF = 100*log(FRED.GDPDEF); FRED.COE = 100*log(FRED.COE); FRED.HOANBS = 100*log(FRED.HOANBS); FRED.PCEC = 100*log(FRED.PCEC); FRED.GPDI = 100*log(FRED.GPDI);

Create a VEC(1) model using the shorthand syntax. Specify the variable names.

Mdl = vecm(7,4,1); Mdl.SeriesNames = FRED.Properties.VariableNames

Mdl =

vecm with properties:

Description: "7-Dimensional Rank = 4 VEC(1) Model with Linear Time Trend"

SeriesNames: "GDP" "GDPDEF" "COE" ... and 4 more

NumSeries: 7

Rank: 4

P: 2

Constant: [7×1 vector of NaNs]

Adjustment: [7×4 matrix of NaNs]

Cointegration: [7×4 matrix of NaNs]

Impact: [7×7 matrix of NaNs]

CointegrationConstant: [4×1 vector of NaNs]

CointegrationTrend: [4×1 vector of NaNs]

ShortRun: {7×7 matrix of NaNs} at lag [1]

Trend: [7×1 vector of NaNs]

Beta: [7×0 matrix]

Covariance: [7×7 matrix of NaNs]

Mdl is a vecm model object. All properties containing NaN values correspond to parameters to be estimated given data.

Estimate the model using the entire data set and the default options. By default, estimate uses the first p = 2 observations as presample data.

EstMdl = estimate(Mdl,FRED.Variables)

EstMdl =

vecm with properties:

Description: "7-Dimensional Rank = 4 VEC(1) Model"

SeriesNames: "GDP" "GDPDEF" "COE" ... and 4 more

NumSeries: 7

Rank: 4

P: 2

Constant: [14.1329 8.77841 -7.20359 ... and 4 more]'

Adjustment: [7×4 matrix]

Cointegration: [7×4 matrix]

Impact: [7×7 matrix]

CointegrationConstant: [-28.6082 -109.555 77.0912 ... and 1 more]'

CointegrationTrend: [4×1 vector of zeros]

ShortRun: {7×7 matrix} at lag [1]

Trend: [7×1 vector of zeros]

Beta: [7×0 matrix]

Covariance: [7×7 matrix]

EstMdl is an estimated vecm model object. It is fully specified because all parameters have known values. By default, estimate imposes the constraints of the H1 Johansen VEC model form by removing the cointegrating trend and linear trend terms from the model. Parameter exclusion from estimation is equivalent to imposing equality constraints to zero.

Generate a numobs-by-7 series of random Gaussian distributed values, where numobs is the number of observations in the data minus p.

numobs = size(FRED,1) - Mdl.P;

rng(1) % For reproducibility

Z = randn(numobs,Mdl.NumSeries);To simulate responses, filter the disturbances through the estimated model. Specify the first p = 2 observations as presample data.

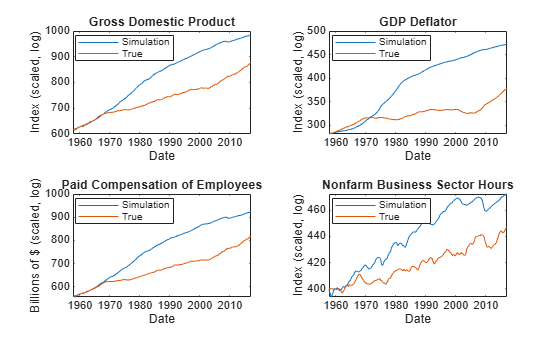

Y = filter(EstMdl,Z,Y0=FRED{1:2,:});Y is a 238-by-7 matrix of simulated responses. Columns correspond to the variable names in EstMdl.SeriesNames.

Plot the simulated and true responses.

figure tiledlayout(2,2) nexttile plot(FRED.Time(3:end),[FRED.GDP(3:end) Y(:,1)]) title("Gross Domestic Product") ylabel("Index (scaled, log)") xlabel("Date") legend("Simulation","True","Location","Best") nexttile plot(FRED.Time(3:end),[FRED.GDPDEF(3:end) Y(:,2)]) title("GDP Deflator") ylabel("Index (scaled, log)") xlabel("Date") legend("Simulation","True","Location","Best") nexttile plot(FRED.Time(3:end),[FRED.COE(3:end) Y(:,3)]) title("Paid Compensation of Employees") ylabel("Billions of $ (scaled, log)") xlabel("Date") legend("Simulation","True","Location","Best") nexttile plot(FRED.Time(3:end),[FRED.HOANBS(3:end) Y(:,4)]) title("Nonfarm Business Sector Hours") ylabel("Index (scaled, log)") xlabel("Date") legend("Simulation","True","Location","Best")

figure tiledlayout(2,2) nexttile plot(FRED.Time(3:end),[FRED.FEDFUNDS(3:end) Y(:,5)]) title("Federal Funds Rate") ylabel("Percent") xlabel("Date") nexttile plot(FRED.Time(3:end),[FRED.PCEC(3:end) Y(:,6)]) title("Consumption Expenditures") ylabel("Billions of $ (scaled, log)") xlabel("Date") nexttile plot(FRED.Time(3:end),[FRED.GPDI(3:end) Y(:,7)]) title("Gross Private Domestic Investment") ylabel("Billions of $ (scaled, log)") xlabel("Date")

Consider this VEC(1) model for three hypothetical response series.

The innovations are multivariate Gaussian with a mean of 0 and the covariance matrix

Create variables for the parameter values.

Adjustment = [-0.3 0.3; -0.2 0.1; -1 0];

Cointegration = [0.1 -0.7; -0.2 0.5; 0.2 0.2];

ShortRun = {[0. 0.1 0.2; 0.2 -0.2 0; 0.7 -0.2 0.3]};

Constant = [-1; -3; -30];

Trend = [0; 0; 0];

Covariance = [1.3 0.4 1.6; 0.4 0.6 0.7; 1.6 0.7 5];Create a vecm model object representing the VEC(1) model using the appropriate name-value pair arguments.

Mdl = vecm('Adjustment',Adjustment,'Cointegration',Cointegration,... 'Constant',Constant,'ShortRun',ShortRun,'Trend',Trend,... 'Covariance',Covariance)

Mdl =

vecm with properties:

Description: "3-Dimensional Rank = 2 VEC(1) Model"

SeriesNames: "Y1" "Y2" "Y3"

NumSeries: 3

Rank: 2

P: 2

Constant: [-1 -3 -30]'

Adjustment: [3×2 matrix]

Cointegration: [3×2 matrix]

Impact: [3×3 matrix]

CointegrationConstant: [2×1 vector of NaNs]

CointegrationTrend: [2×1 vector of NaNs]

ShortRun: {3×3 matrix} at lag [1]

Trend: [3×1 vector of zeros]

Beta: [3×0 matrix]

Covariance: [3×3 matrix]

Mdl is, effectively, a fully specified vecm model object. That is, the cointegration constant and linear trend are unknown. However, they are not needed for simulating observations or forecasting, given that the overall constant and trend parameters are known.

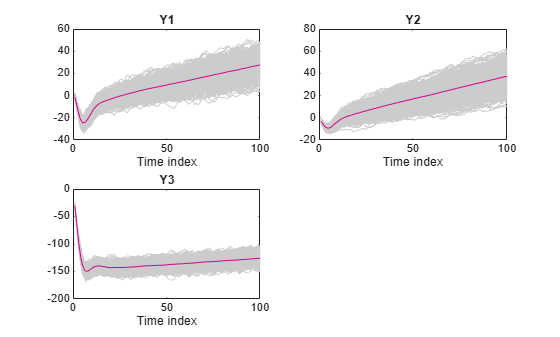

Generate 1000 paths of 100 observations from a 3-D Gaussian distribution. numobs is the number of observations in the data without any missing values.

numobs = 100; numpaths = 1000; rng(1); Z = randn(numobs,Mdl.NumSeries,numpaths);

Filter the disturbances through the estimated model. Return the innovations (scaled disturbances).

[Y,E] = filter(Mdl,Z);

Y and E are 100-by-3-by-1000 matrices of filtered responses and scaled disturbances, respectively.

For each time point, compute the mean vector of the filtered responses among all paths.

MeanFilt = mean(Y,3);

MeanFilt is a 100-by-3 matrix containing the average of the filtered responses at each time point.

Plot the filtered responses and their averages.

figure; for j = 1:Mdl.NumSeries subplot(2,2,j) plot(squeeze(Y(:,j,:)),'Color',[0.8,0.8,0.8]) title(Mdl.SeriesNames{j}); hold on plot(MeanFilt(:,j)); xlabel('Time index') hold off end

Since R2022b

Fit a VEC(1) model to seven macroeconomic series. Then, simulate responses by filtering multiple random paths of Gaussian distributed disturbances through the estimated model. Supply the disturbances in a timetable. This example is based on Fit VEC(1) Model to Matrix of Response Data.

Load and Preprocess Data

Load the Data_USEconVECModel data set.

load Data_USEconVECModel

head(FRED) Time GDP GDPDEF COE HOANBS FEDFUNDS PCEC GPDI

___________ _____ ______ _____ ______ ________ _____ ____

31-Mar-1957 470.6 16.485 260.6 54.756 2.96 282.3 77.7

30-Jun-1957 472.8 16.601 262.5 54.639 3 284.6 77.9

30-Sep-1957 480.3 16.701 265.1 54.375 3.47 289.2 79.3

31-Dec-1957 475.7 16.711 263.7 53.249 2.98 290.8 71

31-Mar-1958 468.4 16.892 260.2 52.043 1.2 290.3 66.7

30-Jun-1958 472.8 16.94 259.9 51.297 0.93 293.2 65.1

30-Sep-1958 486.7 17.043 267.7 51.908 1.76 298.3 72

31-Dec-1958 500.4 17.123 272.7 52.683 2.42 302.2 80

Stabilize all series, except the federal funds rate, by applying the log transform. Scale the resulting series by 100 so that all series are on the same scale.

FRED.GDP = 100*log(FRED.GDP); FRED.GDPDEF = 100*log(FRED.GDPDEF); FRED.COE = 100*log(FRED.COE); FRED.HOANBS = 100*log(FRED.HOANBS); FRED.PCEC = 100*log(FRED.PCEC); FRED.GPDI = 100*log(FRED.GPDI); numobs = height(FRED)

numobs = 240

Prepare Timetable for Estimation

When you plan to supply a timetable directly to estimate, you must ensure it has all the following characteristics:

All selected response variables are numeric and do not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the table.

DTT = rmmissing(FRED); numobs = height(DTT)

numobs = 240

DTT does not contain any missing values.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTT,"quarters")areTimestampsRegular = logical

0

areTimestampsSorted = issorted(DTT.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 0 indicates that the timestamps of DTT are irregular. areTimestampsSorted = 1 indicates that the timestamps are sorted. Macroeconomic series in this example are timestamped at the end of the month. This quality induces an irregularly measured series.

Remedy the time irregularity by shifting all dates to the first day of the quarter.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt; areTimestampsRegular = isregular(DTT,"quarters")

areTimestampsRegular = logical

1

DTT is regular with respect to time.

Fit Model to Data

Create a VEC(1) model using the shorthand syntax. Specify the variable names.

Mdl = vecm(7,4,1); Mdl.SeriesNames = string(FRED.Properties.VariableNames);

Estimate the model. Pass the entire timetable DTT. By default, estimate selects the response variables in Mdl.SeriesNames to fit to the model. Alternatively, you can use the ResponseVariables name-value argument.

EstMdl = estimate(Mdl,DTT);

Simulate Paths of Disturbances

Generate a numobs-by-numseries-by-numpaths array of independent random Gaussian distributed values, where numobs is the number of observations in the data, numseries the number of response series 7, and numpaths is 100. Add the matrices of simulated paths into the data set DTT.

rng(1) % For reproducibility numobs = height(DTT); numseries = EstMdl.NumSeries; numpaths = 100; Z = mvnrnd(zeros(numseries,1),eye(numseries),numobs*numpaths); Z = reshape(Z,numobs,numseries,numpaths); for j = 1:numseries DTT = addvars(DTT,squeeze(Z(:,j,:)), ... NewVariableNames="Z_" + EstMdl.SeriesNames{j}); end head(DTT)

Time GDP GDPDEF COE HOANBS FEDFUNDS PCEC GPDI Z_GDP Z_GDPDEF Z_COE Z_HOANBS Z_FEDFUNDS Z_PCEC Z_GPDI

___________ ______ ______ ______ ______ ________ ______ ______ ____________ ____________ ____________ ____________ ____________ ____________ ____________

01-Jan-1957 615.4 280.25 556.3 400.29 2.96 564.3 435.29 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Apr-1957 615.87 280.95 557.03 400.07 3 565.11 435.54 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Jul-1957 617.44 281.55 558.01 399.59 3.47 566.71 437.32 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Oct-1957 616.48 281.61 557.48 397.5 2.98 567.26 426.27 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Jan-1958 614.93 282.68 556.15 395.21 1.2 567.09 420.02 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Apr-1958 615.87 282.97 556.03 393.76 0.93 568.09 417.59 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Jul-1958 618.76 283.57 558.99 394.95 1.76 569.81 427.67 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Oct-1958 621.54 284.04 560.84 396.43 2.42 571.11 438.2 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

Filter Disturbances Through Model

When you filter disturbances by using a timetable, filter requires a presample. Split the timetable into presample and in-sample data sets. The presample data is the initial EstMdl.P observations, and the in-sample data set contains the remaining observations.

Presample = DTT(1:EstMdl.P,:); InSample = DTT((EstMdl.P + 1):end,:);

Simulate response paths by filtering the in-sample disturbances through the estimated model. Specify the variable names of the disturbance series, the presample data, and the response variable names in the presample.

dnames = string(DTT.Properties.VariableNames); idx = startsWith(dnames,"Z_"); dnames = dnames(idx); Tbl2 = filter(EstMdl,InSample,DisturbanceVariables=dnames, ... Presample=Presample,PresampleResponseVariables=EstMdl.SeriesNames); size(Tbl2)

ans = 1×2

238 28

head(Tbl2)

Time GDP GDPDEF COE HOANBS FEDFUNDS PCEC GPDI Z_GDP Z_GDPDEF Z_COE Z_HOANBS Z_FEDFUNDS Z_PCEC Z_GPDI GDP_Responses GDPDEF_Responses COE_Responses HOANBS_Responses FEDFUNDS_Responses PCEC_Responses GPDI_Responses GDP_Innovations GDPDEF_Innovations COE_Innovations HOANBS_Innovations FEDFUNDS_Innovations PCEC_Innovations GPDI_Innovations

___________ ______ ______ ______ ______ ________ ______ ______ ____________ ____________ ____________ ____________ ____________ ____________ ____________ _____________ ________________ _____________ ________________ __________________ ______________ ______________ _______________ __________________ _______________ __________________ ____________________ ________________ ________________

01-Jul-1957 617.44 281.55 558.01 399.59 3.47 566.71 437.32 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Oct-1957 616.48 281.61 557.48 397.5 2.98 567.26 426.27 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Jan-1958 614.93 282.68 556.15 395.21 1.2 567.09 420.02 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Apr-1958 615.87 282.97 556.03 393.76 0.93 568.09 417.59 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Jul-1958 618.76 283.57 558.99 394.95 1.76 569.81 427.67 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Oct-1958 621.54 284.04 560.84 396.43 2.42 571.11 438.2 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Jan-1959 623.66 284.31 563.55 398.35 2.8 573.62 442.12 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

01-Apr-1959 626.19 284.46 565.91 400.24 3.39 575.54 449.31 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double 1×100 double

Tbl2 is a 238-by-2 matrix of in-sample data, paths of simulated disturbances, paths of filtered responses (variables names appended with _Responses, and paths of innovations (variables with name appended with _Innovations).

rnames = string(Tbl2.Properties.VariableNames); idx = endsWith(rnames,"_Responses"); rnames = rnames(idx); figure tiledlayout(2,2) for j = 1:4 nexttile p1 = plot(Tbl2.Time,Tbl2{:,rnames(j)},Color=[0.5 0.5 0.5]); hold on p2 = plot(Tbl2.Time,Tbl2{:,Mdl.SeriesNames(j)},LineWidth=2); title(Mdl.SeriesNames(j)) xlabel("Date") legend([p1(1) p2],["Simulated" "Observed"]) end

figure tiledlayout(2,2) for j = 5:7 nexttile p1 = plot(Tbl2.Time,Tbl2{:,rnames(j)},Color=[0.5 0.5 0.5]); hold on p2 = plot(Tbl2.Time,Tbl2{:,Mdl.SeriesNames(j)},LineWidth=2); title(Mdl.SeriesNames(j)) xlabel("Date") legend([p1(1) p2],["Simulated" "Observed"]) end

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

filtercomputesYandEusing this process for each pagejinZ.If

Scaleistrue, thenE(:,:,=j)L*Z(:,:,, wherej)L=chol(Mdl.Covariance,'lower'). Otherwise,E(:,:,=j)Z(:,:,. Set et =j)E(:,:,.j)Y(:,:,is yt in this system of equations.j)For variable definitions, see Vector Error-Correction Model.

filtergeneralizessimulate. Both functions filter a disturbance series through a model to produce responses and innovations. However, whereassimulategenerates a series of mean-zero, unit-variance, independent Gaussian disturbancesZto form innovationsE=L*Z,filterenables you to supply disturbances from any distribution.filteruses this process to determine the time origin t0 of models that include linear time trends.If you do not specify

Y0, then t0 = 0.Otherwise,

filtersets t0 tosize(Y0,1)–Mdl.P. Therefore, the times in the trend component are t = t0 + 1, t0 + 2,..., t0 +numobs, wherenumobsis the effective sample size (size(Y,1)afterfilterremoves missing values). This convention is consistent with the default behavior of model estimation in whichestimateremoves the firstMdl.Presponses, reducing the effective sample size. Althoughfilterexplicitly uses the firstMdl.Ppresample responses inY0to initialize the model, the total number of observations inY0andY(excluding missing values) determines t0.

References

[1] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[2] Johansen, S. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models. Oxford: Oxford University Press, 1995.

[3] Juselius, K. The Cointegrated VAR Model. Oxford: Oxford University Press, 2006.

[4] Lütkepohl, H. New Introduction to Multiple Time Series Analysis. Berlin: Springer, 2005.