quantileError

Quantile loss using bag of regression trees

Syntax

Description

err = quantileError(Mdl,X)X to the predicted medians

resulting from applying the bag of regression trees Mdl to

the observations of the predictor data in X.

Mdlmust be aTreeBaggermodel object.The response variable name in

Xmust have the same name as the response variable in the table containing the training data.

err = quantileError(Mdl,X,ResponseVarName)X. ResponseVarName is

the name of the response variable and Mdl.PredictorNames contain

the names of the predictor variables.

err = quantileError(___,Name,Value)Name,Value pair arguments. For example,

specify quantile probabilities, the error type, or which trees to

include in the quantile-regression-error estimation.

Input Arguments

Name-Value Arguments

Output Arguments

Examples

Load the carsmall data set. Consider a model that predicts the fuel economy of a car given its engine displacement, weight, and number of cylinders. Consider Cylinders a categorical variable.

load carsmall

Cylinders = categorical(Cylinders);

X = table(Displacement,Weight,Cylinders,MPG);Train an ensemble of bagged regression trees using the entire data set. Specify 100 weak learners.

rng(1); % For reproducibility Mdl = TreeBagger(100,X,'MPG','Method','regression');

Mdl is a TreeBagger ensemble.

Perform quantile regression, and estimate the MAD of the entire ensemble using the predicted conditional medians.

err = quantileError(Mdl,X)

err = 1.2339

Because X is a table containing the response and commensurate variable names, you do not have to specify the response variable name or data. However, you can specify the response using this syntax.

err = quantileError(Mdl,X,'MPG')err = 1.2339

Load the carsmall data set. Consider a model that predicts the fuel economy of a car given its engine displacement, weight, and number of cylinders.

load carsmall

X = table(Displacement,Weight,Cylinders,MPG);Randomly split the data into two sets: 75% training and 25% testing. Extract the subset indices.

rng(1); % For reproducibility cvp = cvpartition(size(X,1),'Holdout',0.25); idxTrn = training(cvp); idxTest = test(cvp);

Train an ensemble of bagged regression trees using the training set. Specify 250 weak learners.

Mdl = TreeBagger(250,X(idxTrn,:),'MPG','Method','regression');

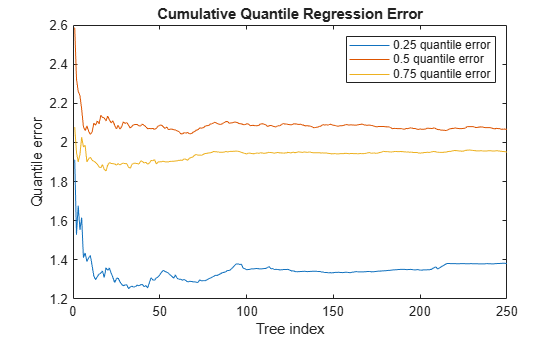

Estimate the cumulative 0.25, 0.5, and 0.75 quantile regression errors for the test set. Pass the predictor data in as a numeric matrix, and the response data in as a vector.

err = quantileError(Mdl,X{idxTest,1:3},MPG(idxTest),'Quantile',[0.25 0.5 0.75],...

'Mode','cumulative');err is a 250-by-3 matrix of cumulative quantile regression errors. Columns correspond to quantile probabilities and rows correspond to trees in the ensemble. The errors are cumulative, so they incorporate aggregated predictions from previous trees. Although, Mdl was trained using a table, if all predictor variables in the table are numeric, then you can supply a matrix of predictor data instead.

Plot the cumulative quantile errors on the same plot.

figure; plot(err); legend('0.25 quantile error','0.5 quantile error','0.75 quantile error'); ylabel('Quantile error'); xlabel('Tree index'); title('Cumulative Quantile Regression Error')

Training using about 60 trees appears to be enough for the first two quartiles, but the third quartile requires about 150 trees.

More About

Tips

To tune the number of trees in the ensemble, set

'Mode','cumulative'and plot the quantile regression errors with respect to tree indices. The maximal number of required trees is the tree index where the quantile regression error appears to level off.To investigate the performance of a model when the training sample is small, use

oobQuantileErrorinstead.

References

[1] Breiman, L. Random Forests. Machine Learning 45, pp. 5–32, 2001.

[2] Meinshausen, N. “Quantile Regression Forests.” Journal of Machine Learning Research, Vol. 7, 2006, pp. 983–999.

Version History

Introduced in R2016b