fgls

Feasible generalized least squares

Syntax

Description

[

returns vectors of coefficient estimates and corresponding standard errors, and the

estimated coefficient covariance matrix, from applying feasible generalized least squares (FGLS) to the multiple linear regression

model coeff,se,EstCoeffCov] = fgls(X,y)y = Xβ +

ε. y is a vector of response data and

X is a matrix of predictor data.

[

returns a table containing FGLS coefficient estimates and corresponding standard errors,

and a table containing the FGLS estimated coefficient covariance matrix, from applying

FGLS to the variables in the input table or timetable. The response variable in the

regression is the last variable, and all other variables are the predictor

variables.CoeffTbl,CovTbl] = fgls(Tbl)

To select a different response variable for the regression, use the

ResponseVariable name-value argument. To select different predictor

variables, use the PredictorNames name-value argument.

[___] = fgls(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)fgls returns the output argument combination for the

corresponding input arguments.

For example,

fgls(Tbl,ResponseVariable="GDP",InnovMdl="H4",Plot="all") provides

coefficient, standard error, and residual mean-squared error (MSE) plots of iterations of

FGLS for a regression model with White’s robust innovations covariance, and the table

variable GDP is the response while all other variables are

predictors.

[___] = fgls(

plots on the axes specified in ax,___,Plot=plot)ax instead of the axes of new figures

when plot is not "off". ax can

precede any of the input argument combinations in the previous syntaxes.

[___,

returns handles to plotted graphics objects when iterPlots] = fgls(___,Plot=plot)plot is not

"off". Use elements of iterPlots to modify

properties of the plots after you create them.

Examples

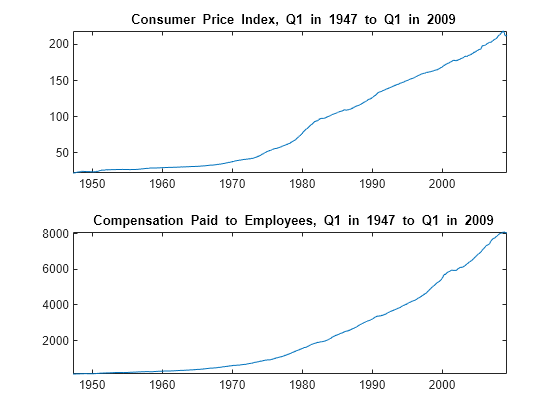

Suppose the sensitivity of the US consumer price index (CPI) to changes in the paid compensation of employees (COE) is of interest.

Load the US macroeconomic data set, which contains the timetable of data DataTimeTable. Extract the COE and CPI series from the table.

load Data_USEconModel.mat

COE = DataTimeTable.COE;

CPI = DataTimeTable.CPIAUCSL;

dt = DataTimeTable.Time;Plot the series.

tiledlayout(2,1) nexttile plot(dt,CPI); title("\bf Consumer Price Index, Q1 in 1947 to Q1 in 2009"); axis tight nexttile plot(dt,COE); title("\bf Compensation Paid to Employees, Q1 in 1947 to Q1 in 2009"); axis tight

The series are nonstationary. Stabilize them by computing their returns.

rCPI = price2ret(CPI); rCOE = price2ret(COE);

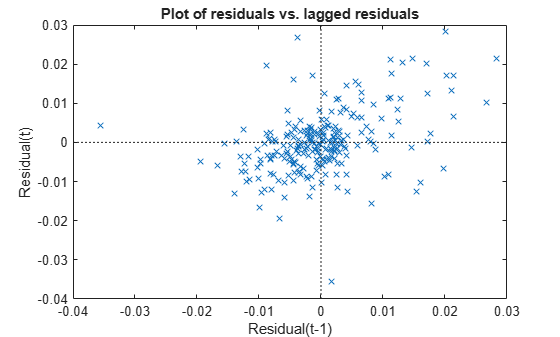

Regress rCPI onto rCOE including an intercept to obtain ordinary least squares (OLS) estimates, standard errors, and the estimated coefficient covariance. Generate a lagged residual plot.

Mdl = fitlm(rCOE,rCPI); clmCoeff = Mdl.Coefficients.Estimate

clmCoeff = 2×1

0.0033

0.3513

clmSE = Mdl.Coefficients.SE

clmSE = 2×1

0.0010

0.0490

CLMEstCoeffCov = Mdl.CoefficientCovariance

CLMEstCoeffCov = 2×2

0.0000 -0.0000

-0.0000 0.0024

figure

plotResiduals(Mdl,"lagged")

The residual plot exhibits an upward trend, which suggests that the innovations comprise an autoregressive process. This violates one of the classical linear model assumptions. Consequently, hypothesis tests based on the regression coefficients are incorrect, even asymptotically.

Estimate the regression coefficients, standard errors, and coefficient covariances using FGLS. By default, fgls includes an intercept in the regression model and imposes an AR(1) model on the innovations.

[coeff,se,EstCoeffCov] = fgls(rCPI,rCOE)

coeff = 2×1

0.0148

0.1961

se = 2×1

0.0012

0.0685

EstCoeffCov = 2×2

0.0000 -0.0000

-0.0000 0.0047

Row 1 of the outputs corresponds to the intercept and row 2 corresponds to the coefficient of rCOE.

If the COE series is exogenous with respect to the CPI, then the FGLS estimates coeff are consistent and asymptotically more efficient than the OLS estimates.

Load the US macroeconomic data set, which contains the timetable of data DataTimeTable.

load Data_USEconModelStabilize all series by computing their returns.

RDT = price2ret(DataTimeTable);

RDT is a timetable of returns of all variables in DataTimeTable. The price2ret function conserves variable names.

Estimate the regression coefficients, standard errors, and the coefficient covariance matrix using FGLS. Specify the response and predictor variable names.

[CoeffTbl,CoeffCovTbl] = fgls(RDT,ResponseVariable="CPIAUCSL",PredictorVariables="COE")

CoeffTbl=2×2 table

Coeff SE

__________ _________

Const 6.2416e-05 1.336e-05

COE 0.20562 0.055615

CoeffCovTbl=2×2 table

Const COE

___________ ___________

Const 1.7848e-10 -5.6329e-07

COE -5.6329e-07 0.003093

When you supply a table or timetable of data, fgls returns tables of estimates.

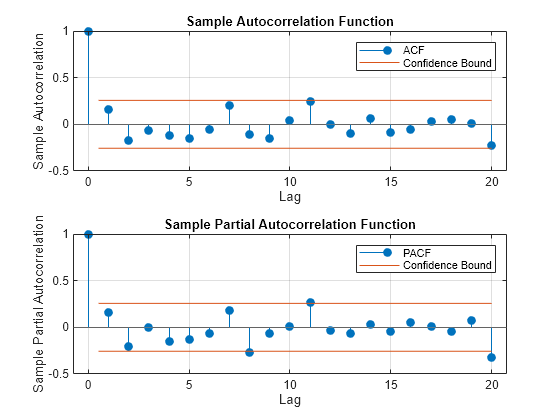

Suppose the sensitivity of the US consumer price index (CPI) to changes in the paid compensation of employees (COE) is of interest. This example expands on the analysis outlined in the example Estimate FGLS Coefficients and Uncertainty Measures.

Load the US macroeconomic data set.

load Data_USEconModelThe series are nonstationary. Stabilize them by applying the log, and then the first difference.

LDT = price2ret(Data); rCOE = LDT(:,1); rCPI = LDT(:,2);

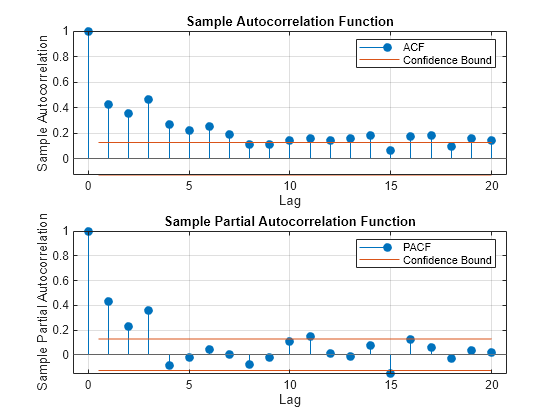

Regress rCPI onto rCOE, which includes an intercept to obtain OLS estimates. Plot correlograms for the residuals.

Mdl = fitlm(rCOE,rCPI); u = Mdl.Residuals.Raw; figure; subplot(2,1,1) autocorr(u); subplot(2,1,2); parcorr(u);

The correlograms suggest that the innovations have significant AR effects. According to Box-Jenkins methodology, the innovations seem to comprise an AR(3) series. For details, see Programmatically Select ARIMA Model for Time Series Using Box-Jenkins Methodology.

Estimate the regression coefficients using FGLS. By default, fgls assumes that the innovations are autoregressive. Specify that the innovations are AR(3) by using the ARLags name-value argument, and print the final estimates to the command window by using the Display name-value argument.

fgls(rCPI,rCOE,ARLags=3,Display="final");OLS Estimates:

| Coeff SE

------------------------

Const | 0.0122 0.0009

x1 | 0.4915 0.0686

FGLS Estimates:

| Coeff SE

------------------------

Const | 0.0148 0.0012

x1 | 0.1972 0.0684

If the COE rate series is exogenous with respect to the CPI rate, the FGLS estimates are consistent and asymptotically more efficient than the OLS estimates.

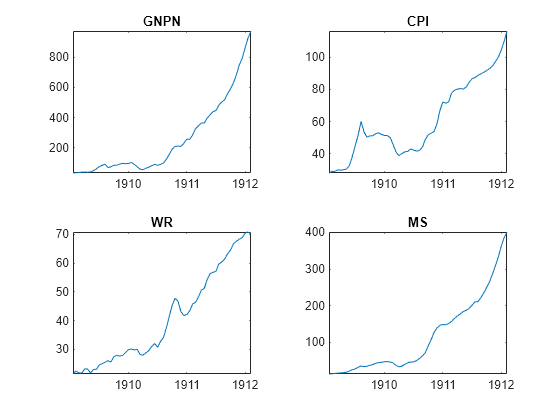

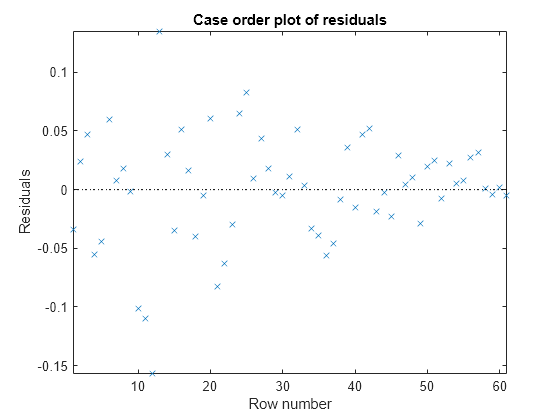

Model the nominal GNP GNPN growth rate accounting for the effects of the growth rates of the consumer price index CPI, real wages WR, and the money stock MS. Account for classical linear model departures.

Load the Nelson-Plosser data set, which contains the data in the table DataTable. Remove all observations containing at least one missing value.

load Data_NelsonPlosser

DT = rmmissing(DataTable);

T = height(DT); Plot the series.

predNames = ["CPI" "WR" "MS"]; tiledlayout(2,2) for j = ["GNPN" predNames] nexttile plot(DT{:,j}); xticklabels(DT.Dates) title(j); axis tight end

All series appear nonstationary.

For each series, compute the returns.

RetDT = price2ret(DT);

RetTT is a timetable of the returns of the variables in TT. The variables names are conserved.

Regress the GNPN rate onto the CPI, WR, and MS rates. Examine a scatter plot and correlograms of the residuals.

Mdl = fitlm(RetDT,ResponseVar="GNPN",PredictorVar=predNames); figure plotResiduals(Mdl,"caseorder"); axis tight

figure tiledlayout(2,1) nexttile autocorr(Mdl.Residuals.Raw); nexttile parcorr(Mdl.Residuals.Raw);

The residuals appear to flare in, which is indicative of heteroscedasticity. The correlograms suggest that there is no autocorrelation.

Estimate FGLS coefficients by accounting for the heteroscedasticity of the residuals. Specify that the estimated innovation covariance is diagonal with the squared residuals as weights (that is, White's robust estimator H0).

fgls(RetDT,ResponseVariable="GNPN",PredictorVariables=predNames, ... InnovMdl="HC0",Display="final");

OLS Estimates:

| Coeff SE

-------------------------

Const | -0.0076 0.0085

CPI | 0.9037 0.1544

WR | 0.9036 0.1906

MS | 0.4285 0.1379

FGLS Estimates:

| Coeff SE

-------------------------

Const | -0.0102 0.0017

CPI | 0.8853 0.0169

WR | 0.8897 0.0294

MS | 0.4874 0.0291

Create this regression model with ARMA(1,2) errors, where is Gaussian with mean 0 and variance 1.

beta = [2 3];

phi = 0.2;

theta = [-0.3 0.1];

Mdl = regARIMA(AR=phi,MA=theta,Intercept=1, ...

Beta=beta,Variance=1);Mdl is a regARIMA model. You can access its properties using dot notation.

Simulate 500 periods of 2-D standard Gaussian values for , and then simulate responses using Mdl.

numObs = 500;

rng(1); % For reproducibility

X = randn(numObs,2);

y = simulate(Mdl,numObs,X=X);fgls supports AR(p) innovation models. You can convert an ARMA model polynomial to an infinite-lag AR model polynomial using arma2ar. By default, arma2ar returns the coefficients for the first 10 terms. After the conversion, determine how many lags of the resulting AR model are practically significant by checking the length of the returned vector of coefficients. Choose the number of terms that exceed 0.00001.

format long

arParams = arma2ar(phi,theta)arParams = 1×3

-0.100000000000000 0.070000000000000 0.031000000000000

arLags = sum(abs(arParams) > 0.00001);

format shortSome of the parameters have small magnitude. You might want to reduce the number of lags to include in the innovations model for fgls.

Estimate the coefficients and their standard errors using FGLS and the simulated data. Specify that the innovations comprise an AR(arLags) process.

[coeff,~,EstCoeffCov] = fgls(X,y,InnovMdl="AR",ARLags=arLags)coeff = 3×1

1.0372

2.0366

2.9918

EstCoeffCov = 3×3

0.0026 -0.0000 0.0001

-0.0000 0.0022 0.0000

0.0001 0.0000 0.0024

The estimated coefficients are close to their true values.

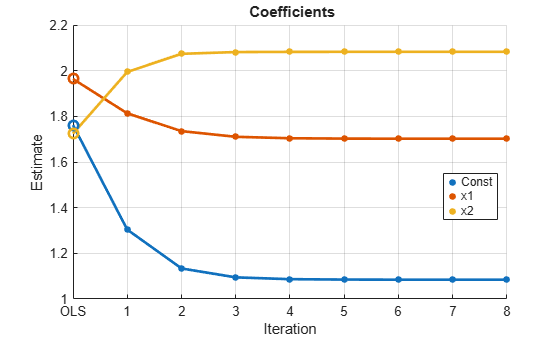

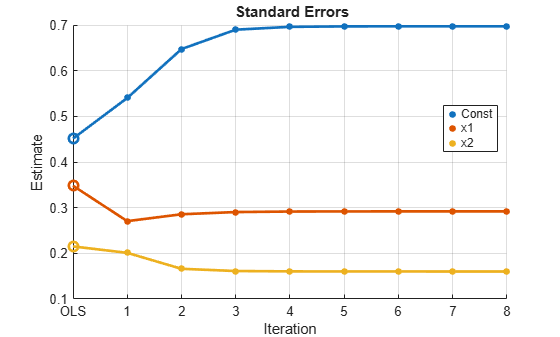

This example expands on the analysis in Estimate FGLS Coefficients of Models Containing ARMA Errors. Create this regression model with ARMA(1,4) errors, where is Gaussian with mean 0 and variance 1.

beta = [1.5 2]; phi = 0.9; theta = [-0.4 0.2]; Mdl = regARIMA(AR=phi,MA=theta,MALags=[1 4],Intercept=1,Beta=beta,Variance=1);

Suppose the distribution of the predictors is

Simulate 30 periods from , and then simulate 30 corresponding responses from the regression model with ARMA errors Mdl.

numObs = 30;

rng(1); % For reproducibility

muX = [-1 1];

sigX = [0.5 1];

X = randn(numObs,numel(beta)).*sigX + muX;

y = simulate(Mdl,numObs,X=X);Convert the ARMA model polynomial to an infinite-lag AR model polynomial using arma2ar. By default, arma2ar returns the coefficients for the first 10 terms. Find the number of terms that exceed 0.00001.

arParams = arma2ar(phi,theta); arLags = sum(abs(arParams) > 1e-5);

Estimate the regression coefficients by using eight iterations of FGLS, and specify the number of lags in the AR innovation model (arLags). Also, specify to plot the coefficient estimates and their standard errors for each iteration, and to display the final estimates and the OLS estimates in tabular form.

[coeff,~,EstCoeffCov] = fgls(X,y,InnovMdl="AR",ARLags=arLags, ... NumIter=8,Plot=["coeff" "se"],Display="final");

OLS Estimates:

| Coeff SE

------------------------

Const | 1.7619 0.4514

x1 | 1.9637 0.3480

x2 | 1.7242 0.2152

FGLS Estimates:

| Coeff SE

------------------------

Const | 1.0845 0.6972

x1 | 1.7020 0.2919

x2 | 2.0825 0.1603

The algorithm seems to converge after the four iterations. The FGLS estimates are closer to the true values than the OLS estimates.

Properties of iterative FGLS estimates in finite samples are difficult to establish. For asymptotic properties, one iteration of FGLS is sufficient, but fgls supports iterative FGLS for experimentation.

If the estimates or standard errors show instability after successive iterations, then the estimated innovations covariance might be ill conditioned. Consider scaling the residuals by using the ResCond name-value argument to improve the conditioning of the estimated innovations covariance.

Input Arguments

Name-Value Arguments

Output Arguments

More About

Tips

To obtain standard generalized least squares (GLS) estimates:

To obtain weighted least squares (WLS) estimates, set the

InnovCov0name-value argument to a vector of inverse weights (e.g., innovations variance estimates).In specific models and with repeated iterations, scale differences in the residuals might produce a badly conditioned estimated innovations covariance and induce numerical instability. Conditioning improves when you set

ResCond=true.

Algorithms

In the presence of nonspherical innovations, GLS produces efficient estimates relative to OLS and consistent coefficient covariances, conditional on the innovations covariance. The degree to which

fglsmaintains these properties depends on the accuracy of both the model and estimation of the innovations covariance.Rather than estimate FGLS estimates the usual way,

fglsuses methods that are faster and more stable, and are applicable to rank-deficient cases.Traditional FGLS methods, such as the Cochrane-Orcutt procedure, use low-order, autoregressive models. These methods, however, estimate parameters in the innovations covariance matrix using OLS, where

fglsuses maximum likelihood estimation (MLE) [2].

References

[1] Cribari-Neto, F. "Asymptotic Inference Under Heteroskedasticity of Unknown Form." Computational Statistics & Data Analysis. Vol. 45, 2004, pp. 215–233.

[2] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[3] Judge, G. G., W. E. Griffiths, R. C. Hill, H. Lϋtkepohl, and T. C. Lee. The Theory and Practice of Econometrics. New York, NY: John Wiley & Sons, Inc., 1985.

[4] Kutner, M. H., C. J. Nachtsheim, J. Neter, and W. Li. Applied Linear Statistical Models. 5th ed. New York: McGraw-Hill/Irwin, 2005.

[5] MacKinnon, J. G., and H. White. "Some Heteroskedasticity-Consistent Covariance Matrix Estimators with Improved Finite Sample Properties." Journal of Econometrics. Vol. 29, 1985, pp. 305–325.

[6] White, H. "A Heteroskedasticity-Consistent Covariance Matrix and a Direct Test for Heteroskedasticity." Econometrica. Vol. 48, 1980, pp. 817–838.