psaspeed2rate

Single monthly mortality rate given PSA speed

Description

Examples

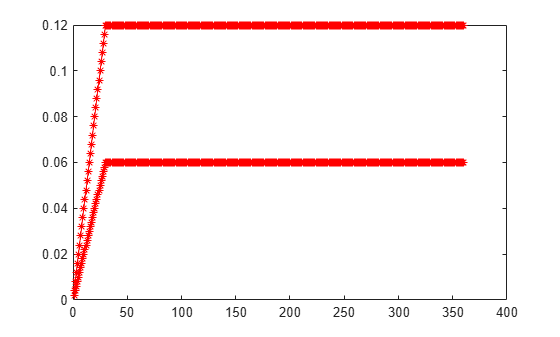

This example shows how to compute the prepayment and mortality rates, given a mortgage-backed security with annual speed set at the PSA default benchmark.

PSASpeed = [100 200]; [CPRPSA, SMMPSA]= psaspeed2rate(PSASpeed)

CPRPSA = 360×2

0.0020 0.0040

0.0040 0.0080

0.0060 0.0120

0.0080 0.0160

0.0100 0.0200

0.0120 0.0240

0.0140 0.0280

0.0160 0.0320

0.0180 0.0360

0.0200 0.0400

0.0220 0.0440

0.0240 0.0480

0.0260 0.0520

0.0280 0.0560

0.0300 0.0600

⋮

SMMPSA = 360×2

0.0002 0.0003

0.0003 0.0007

0.0005 0.0010

0.0007 0.0013

0.0008 0.0017

0.0010 0.0020

0.0012 0.0024

0.0013 0.0027

0.0015 0.0031

0.0017 0.0034

0.0019 0.0037

0.0020 0.0041

0.0022 0.0044

0.0024 0.0048

0.0025 0.0051

⋮

% view the plot of the output

psaspeed2rate(PSASpeed)

Input Arguments

Output Arguments

More About

References

[1] PSA Uniform Practices, SF-49

Version History

Introduced before R2006a