categoryReturnsChart

Description

categoryReturnsChart( creates a

horizontal bar chart of portfolio and benchmark category returns, aggregated over all time

periods using a BrinsonPAObj)brinsonAttribution

object.

h = categoryReturnsChart(ax,BrinsonPAObj)h.

Examples

This example shows how to create a brinsonAttribution object that you can then use with the categoryReturnsChart function to generate a bar chart of category returns.

Prepare Data

Create a table for the monthly prices for four assets.

GM =[17.82;22.68;19.37;20.28]; HD = [39.79;39.12;40.67;40.96]; KO = [38.98;39.44;40.00;40.20]; PG = [56.38;57.08;57.76;55.54]; MonthlyPrices = table(GM,HD,KO,PG);

Use tick2ret to define the monthly returns.

MonthlyReturns = tick2ret(MonthlyPrices.Variables)'; [NumAssets,NumPeriods] = size(MonthlyReturns);

Define the periods.

Period = ones(NumAssets*NumPeriods,1); for k = 1:NumPeriods Period(k*NumAssets+1:end,1) = Period(k*NumAssets,1) + 1; end

Define the categories (sectors) for the four assets.

Name = repmat(string(MonthlyPrices.Properties.VariableNames(:)),NumPeriods,1); Categories = repmat(categorical([ ... "Consumer Discretionary"; ... "Consumer Discretionary"; ... "Consumer Staples"; ... "Consumer Staples"]),NumPeriods,1);

Define benchmark and portfolio weights.

BenchmarkWeight = repmat(1./NumAssets.*ones(NumAssets, 1),NumPeriods,1); PortfolioWeight = repmat([1;0;1;1]./3,NumPeriods,1);

Create AssetTable Input

Create AssetTable as the input for the brinsonAttribution object.

AssetTable = table(Period, Name, ... MonthlyReturns(:), Categories, PortfolioWeight, BenchmarkWeight, ... VariableNames=["Period","Name","Return","Category","PortfolioWeight","BenchmarkWeight"])

AssetTable=12×6 table

Period Name Return Category PortfolioWeight BenchmarkWeight

______ ____ _________ ______________________ _______________ _______________

1 "GM" 0.27273 Consumer Discretionary 0.33333 0.25

1 "HD" -0.016838 Consumer Discretionary 0 0.25

1 "KO" 0.011801 Consumer Staples 0.33333 0.25

1 "PG" 0.012416 Consumer Staples 0.33333 0.25

2 "GM" -0.14594 Consumer Discretionary 0.33333 0.25

2 "HD" 0.039622 Consumer Discretionary 0 0.25

2 "KO" 0.014199 Consumer Staples 0.33333 0.25

2 "PG" 0.011913 Consumer Staples 0.33333 0.25

3 "GM" 0.04698 Consumer Discretionary 0.33333 0.25

3 "HD" 0.0071306 Consumer Discretionary 0 0.25

3 "KO" 0.005 Consumer Staples 0.33333 0.25

3 "PG" -0.038435 Consumer Staples 0.33333 0.25

Create brinsonAttribution Object

Use brinsonAttribution to create the brinsonAttribution object.

BrinsonPAobj = brinsonAttribution(AssetTable)

BrinsonPAobj =

brinsonAttribution with properties:

NumAssets: 4

NumPortfolioAssets: 3

NumBenchmarkAssets: 4

NumPeriods: 3

NumCategories: 2

AssetName: [4×1 string]

AssetReturn: [4×3 double]

AssetCategory: [4×3 categorical]

PortfolioAssetWeight: [4×3 double]

BenchmarkAssetWeight: [4×3 double]

PortfolioCategoryReturn: [2×3 double]

BenchmarkCategoryReturn: [2×3 double]

PortfolioCategoryWeight: [2×3 double]

BenchmarkCategoryWeight: [2×3 double]

PortfolioReturn: 0.0598

BenchmarkReturn: 0.0540

ActiveReturn: 0.0059

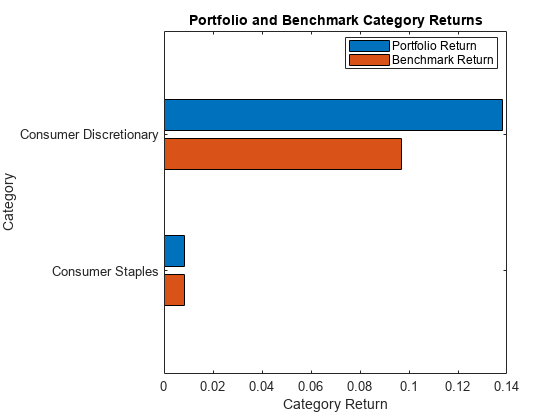

Generate Horizontal Bar Chart for Category Returns

Use the brinsonAttribution object with categoryReturnsChart to generate a horizontal bar chart of portfolio and benchmark category returns, aggregated over all time periods.

categoryReturnsChart(BrinsonPAobj)

Input Arguments

Output Arguments

Version History

Introduced in R2023a